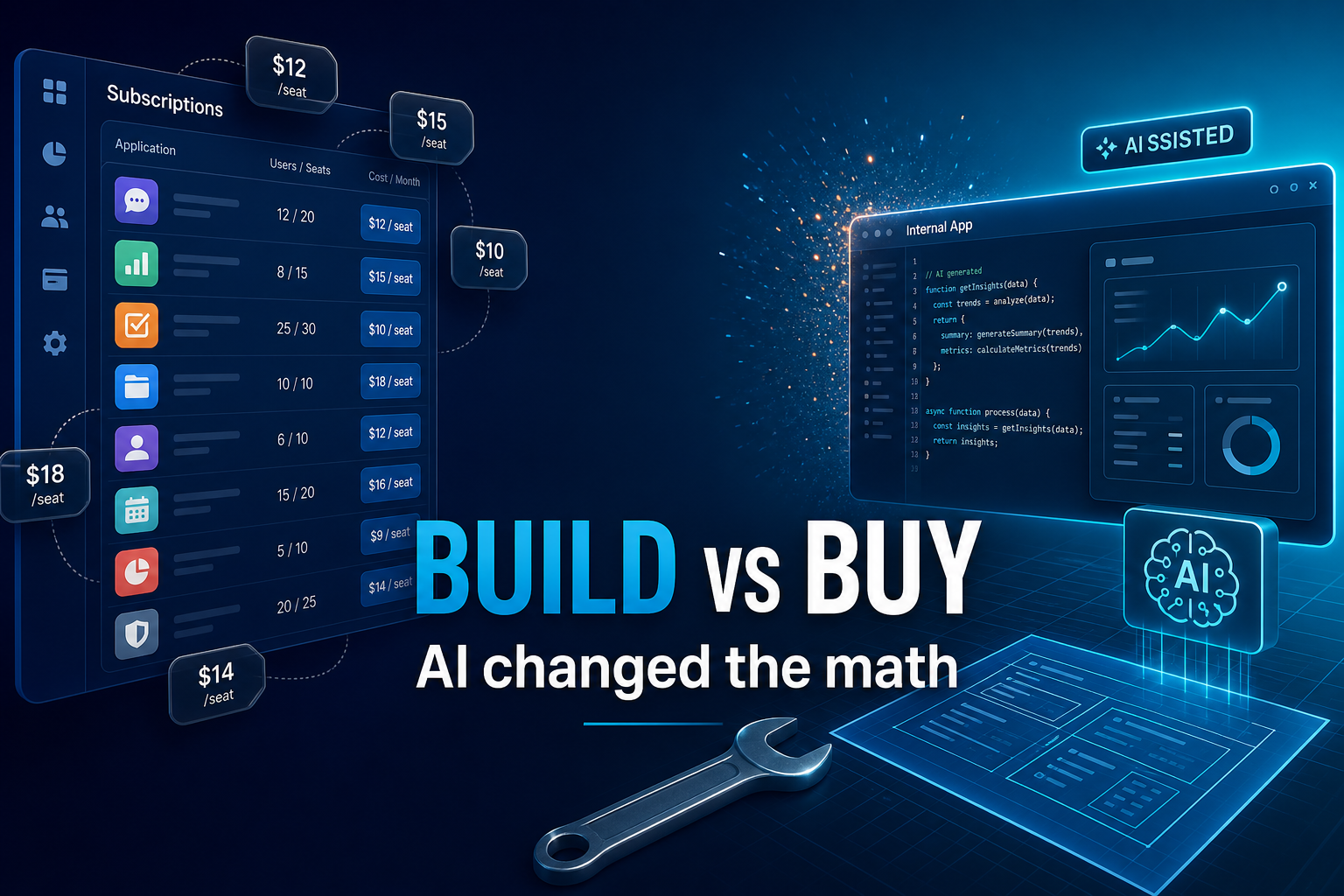

How AI Is Letting Businesses Build Software In-House — and Why SaaS Vendors Should Pay Attention

For two decades, buying SaaS was the safe default. AI-assisted development has not killed software vendors—it has moved the line on what is worth building yourself.

For most of the 2010s, the internal-software playbook was boring in a useful way. You bought subscriptions, accepted an 80% fit, and waited two weeks for procurement. Building in-house meant a six-month queue and a dedicated squad. Unless the workflow was core to your business, buy won.

That math is changing.

The old equation broke quietly, then all at once

AI did not invent custom software. It shortened the path to a working build—especially for the messy middle: approval chains, ops dashboards, one-off integrations, the five-step process your vendor will never prioritize on a roadmap.

Diagram

When build time starts to look like buy time, the question stops being “Can we afford engineers?” and becomes “Is this workflow generic enough to rent?”

That is where seat-based SaaS feels pressure—not because every company will rip out Salesforce next quarter, but because the long tail of per-seat tools is easier to replace than it was eighteen months ago.

What changed in the builder’s toolbox

Three things matured in parallel, and they compound:

Layer

What it does

Why it matters

Inline assistants

Completion inside the IDE

Less boilerplate, faster tests

Codebase-aware agents

Multi-file refactors, repo context

Internal tools that touch real APIs

App generators

Low-code and “vibe” platforms

Ops and finance ship admin UIs without a product team

Copilot-style tools are already common in large enterprises. Cursor sits alongside them in many shops—Copilot for standardized rollout, Cursor for engineers who live in multi-file changes. The shift that matters for SaaS is not autocomplete. It is agents that plan, edit, run, and iterate—the gap between a Jira ticket and a screen someone can click.

Diagram

What the surveys actually say

Twitter and LinkedIn were full of “we replaced X over a weekend” posts long before finance teams felt it. In 2026, vendors started publishing numbers you can cite in a board deck.

35% of teams had already replaced at least one SaaS tool with something they built

78% expect to build more internal tools in 2026

Pressure shows up first in workflow automation and internal admin, then CRM, BI, project management, and support tooling

Retool’s CEO called enterprise app generation a threat to traditional SaaS because rented software forces you to work the vendor’s way. Whether you agree with the framing or not, the direction matches what we hear from mid-market teams—roughly 50 to 300 people, big enough for painful sprawl, small enough that one strong engineer plus AI can beat a procurement cycle.

Three public stories worth reading closely

Klarna: consolidation, not a chatbot CRM

Klarna drew attention when CEO Sebastian Siemiatkowski discussed pulling back from platforms like Salesforce and Workday and consolidating a reported ~1,200 applications toward an internal stack—including a Neo4j knowledge graph. The point was not “put the CRM in ChatGPT.”

In a thread on X, Siemiatkowski walked back the circus that followed a leaked investor call. The work was about unifying data and knowledge, then shipping interfaces faster with tools like Cursor. He expects fewer, larger SaaS hubs—not zero software.

What we take from it: the strategic move is often data unification plus a custom interaction layer. That displaces point solutions even when core ERP or CRM categories stay partially on vendor rails.

Shopify: AI as a baseline, not a hackathon prize

In April 2025, Tobi Lütke told staff that reflexive AI use is now a baseline expectation. Before asking for headcount, teams need to show why AI cannot do the work. Usage feeds performance reviews. Lütke cited large speedups in translations and refactors in replies on X and trade press.

Shopify is still a product company selling to merchants. Internally, though, AI is treated like electricity—expected, measured, wired into how they ship. That culture is what makes another vendor seat harder to justify.

Harmonic: when support latency costs more than building

Retool’s report describes Harmonic replacing a $20,000-per-year tool because vendor support was slower than rebuilding—then growing to 33 internal apps tied into Salesforce, Gong, Slack, and internal APIs, with audit logs and RBAC. The cultural shift was simple: “Why can’t we just build this?”

That is churn driven by time-to-solution, not a keynote about AGI.

Markets: agents and the per-seat story

Even if you are not Klarna, public markets have started pricing displacement risk. After Anthropic’s agentic releases in early 2026, software indices sold off hard—commentators called it “Software-mageddon” as investors asked whether agents reduce the seats required to run workflows (FinancialContent). Every tick does not equal lost revenue, but boards are now asking why seat counts should grow when agents can execute multi-step tasks across existing UIs.

Which SaaS categories feel the heat first?

Not every category is equally exposed. This is a working map, not a verdict:

Diagram

Teams often build when the pain is specific: internal admin and approvals, warehouse-fed dashboards, glue between systems they already pay for, support macros tied to product data, a CRM view for one business unit.

They still buy when liability and regulation sit with the vendor: payroll and statutory reporting, identity at enterprise scale, payments rails, deep vertical compliance.

AI makes the middle layer easier to build—the same layer where vendors earned margin on “good enough.”

Shadow IT is the part nobody puts in the keynote

Speed without ownership is how you end up with dozens of tools nobody maintains. Retool’s survey noted many builds happening outside official procurement—ops and finance shipping fixes before IT catches up. We see the same pattern:

A team buys SaaS and hits a workflow ceiling.

An engineer ships an internal tool over a weekend with AI assist.

Neighbors copy it because it works.

Nobody owns SSO, audit trails, or retirement.

An incident surfaces “production” spreadsheets with API keys.

AI accelerates step two. It does not remove step four. Treat in-house builds like product launches: named owner, SLA, security review, retirement plan.

Why teams leave vendors (it is not always price)

Replaceability is rarely about license cost alone. Common triggers:

Data is hard to export without professional services.

You pay for a hundred seats to unlock one API.

Your process has five steps; the product is built for fifty.

Integrations become a chain of Zapier folklore nobody can debug.

Builds work when the problem is your process, your data, your exceptions. They fail when you need a regulated commodity with liability transfer. Practitioners are honest about the tradeoff: AI-generated code can be harder to debug, so net gains are real but not always the headline multiplier.

A practical decision framework

Use this at the next architecture review:

Diagram

Three questions worth writing down:

If we stopped paying this vendor tomorrow, what breaks—and is that acceptable?

Is the advantage in the UI, or in the data model and integrations?

Who maintains this in year two? AI writes version one; humans own version two through ten.

What this means for SaaS vendors

Incumbents are not standing still. Survivors will likely:

Become data hubs, not just feature bundles

Ship agents inside the product instead of selling seats alone

Move toward usage or outcome pricing

Own compliance narratives customers cannot cheaply replicate

Thin point solutions with slow support look most like Harmonic’s replacement story.

What this means for your organization

The opportunity is not “fire all vendors.” It is selective building with guardrails:

Do

Avoid

A small internal platform—auth, logging, deploy templates

Every team picking its own stack

Governed builders (reviewed repos or Retool-class tools)

Production spreadsheets with API keys

Proven SaaS for ERP, payroll, identity

Rebuilding regulated cores for sport

Measure time saved against maintenance hours

Celebrating demos without owners

Connect builds to ERP or warehouse truth

Another silo of master data

We see the healthiest pattern in clients on ERPNext or hybrid ERP stacks: AI speeds the last mile—portals, approvals, field dashboards—while financial and inventory truth stays in governed systems of record.

Closing thought

AI makes in-house software plausible for more workflows. SaaS is not vanishing; it is segmenting. Commodity capabilities stay rented. Differentiated workflows get built. Platforms that own unified data may grow stronger, not weaker.

The teams that win are not the ones that ship the most demos. They are the ones that pair speed with integration discipline, security, and ownership—the same qualities that separated good ERP programs from expensive shelfware long before ChatGPT.